Today, in January 2020, we are in a market with a lot of skinny deals. Thin margins with a lot of hope embedded in the purchase prices are common. Liquidity is abundant meaning you rarely get paid for providing it. This is one reason why I’m sourcing performing loans at reasonable loan to values. It is hard to get excited about high single digit returns, but there are markets where principal protection is paramount and there are markets where capital appreciation is the name of the game. Performing first mortgages offer downside protection and are otherwise self-liquidating.

Today, I have a story about a different market in a different time. Margins were fat and liquidity was thin. It was the perfect market for those with a market maker´s mindset. What people forget is that doing deals 9-10 years ago took courage. It was contrarian. Just as we have to be independent minded today (willing to pass on many deals), so too did we have to be independent-minded then (buying when others were blindly selling).

In April 2012, I identified an investment in a senior community in Lake San Marcos, San Diego County. It’s useful to get an understanding for the product type and its client. This community is a mix of senior housing product that provides its residents with meals, linen service, on site staff etc. It’s costly. Because of the nature of the clientele, there is some level of natural turnover as people pass away or move into full service assisted living communities. One resident told me confidently that he was only moving out feet first.

The community offered five floor plans.

1 bedroom, 1 bath, 660 Square feet

1 bedroom, 1 bath, 660 Square feet

2 bedroom, 2 bath, 962 square feet

2 bedroom, 2 bath, 1034 square feet

2 bedroom, 2 bath, 1030 square feet

The differences between each of the 1 bedroom units are minimal and the differences among each of the 2 bedrooms units are also minimal. Part of what makes condos interesting is, sure floor plans matter and the condition of a unit matters, but locations and views matter as well and they vary dramatically creating occasional mispricings. Therefore though these are all commodities, even two model matches are heterogenous commodities with different underlying values.

Ok, back to 2012, picture the circumstances. The Great Financial Crisis (GFC) has destroyed home values. There is natural turnover in this senior community. Heirs inherit property and are anchored to old property prices. $160,000, $150,000 etc. But there’s a catch. These apartments are not financeable. They are also costly, with HOA fees running nearly $2,000 per month per unit to cover all of the services provided. Listing agents of unrenovated units likely suggested some renovations to get the unit sold; many heirs hold off making renovations. Renovated or better-located units within the community then sell first.

Anchoring to prior pre-GFC prices hurts heirs. They slowly lower their prices. Too slowly. Death by a thousand cuts. Their listings get stale. Inventory builds. Meanwhile every month they stroke a check to float the HOA fees for services they aren’t using on vacant apartments they aren´t living in. Finally there’s a shift in their mindset. But by the time they realized that they should have previously made improvements to their units, many of them can´t afford to, having gone out of pocket thousands of dollars in HOA fees.

With dozens of unit owners following the same pattern, downward pricing pressure intensifies. No longer do they view these apartments as assets they have inherited but as liabilities they are stuck with! They compete with one another lowering prices hoping to be the next unit to sell. Inventory continues to build faster than it sells. Many people that historically moved into the community would first sell their house, collect a big check and then purchase all cash in this senior community. Were these would be buyers waiting for their house prices to bounce back first?

Enter Bob (dramatic pause). I examined the inventory turn rates and spoke with residents, management and brokers. Demand for two bedroom units had always been higher than one bedroom units. While there was still a glut of 1 bedrooms in 2012 there were only a few 2 bedrooms available. The 2 bedroom inventory had slowly been absorbed. I found that there were only three 2 bedroom units for sale asking $39,000, $40,000, and $190,000. Odd. The $190,000 unit, which was renovated, was in escrow and was listed by an agent that had sold dozens of units within the community over the years. Hmmm.

I felt that this broker might have the buyers for this product that the other brokers lacked. An MLS search indicated that these $40,000 units were about the cheapest 2 bedroom asking prices within this community since data began to be uploaded into MLS in 1995. Back then, these condo’s traded for between $80,000 and $100,000.

If I took the offer at $39,000 and $40,000, I would have absorbed all of the unrenovated 2 bedroom inventory on the market. I could then turn it into a new product, a renovated unit. I then had plenty of room for margin. Liquidity was low but spreads were very high. This was the perfect market to act as a market maker. I bid below the offer prices and proceeded to purchase the two condominiums for an average price of $36,250. Why was I able to purchase condos for less than the price of a pre-HUD singlewide trailer around the corner from the property? Again I found an interesting set of circumstances involving:

1. Forced/capitulating sellers

2. Absent buyers

3. A vicious downward pricing spiral amplifying the spreads between renovated and un-renovated units

4. An opportunity to arbitrage these spreads

5. Asymmetric information with one listing agent having a large number of buyers for this product

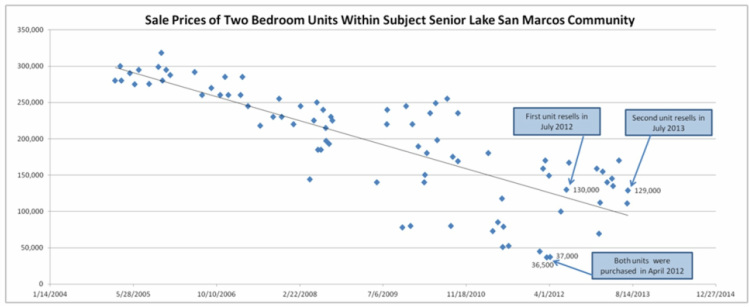

A scatter diagram of sales of two bedroom units between 2005 and 2012 shows a downward trajectory of pricing after 2005. Over time variance among the sales prices also increases. Buyers were paying up for renovated units and passing on original units.

As you can see on the graph, our purchase of the two remaining low price two-bedroom units ticked the bottom of the market within the community. We renovated the units and listed them with the agent who had brokered the sale of dozens of homes within the community.

Money is always made on the buy. I pulled no rabbits out of hats. The entire trade took longer than I would have liked, but a bargain purchase price created downside protection. I quickly sold one unit for $130,000 recapturing all of the capital employed on the purchase, renovation and carry on both units and creating a pretax reserve of $55,000. It would be a year before I sold the second unit. In my next post, I will discuss what happened outside the window to this second unit and how I solved the buyer objections created by the “spectacle” outside this unit´s window.

Recent Comments