The Risk Free Rate of return underpins the value of trillions of dollars of assets. As the “risk free” return edges lower, it induces us to purchase risk assets requiring higher expected returns. Because the Dollar is the global reserve currency, the United States Treasury yield curve illustrates the “risk free rate.” Some financial models might use the 3 month T bill, others the 2 year, 5 year, 10 year or 30 year bond but which term Treasury note is most appropriate for determining the risk free rate doesn’t matter for our purposes today.

What matters is, the Risk Free Rate is broken. I am borrowing Jim Grant’s phrase–Return Free Risk-here to describe the purchase of intermediate or long-term Treasuries today. Historically long-term treasuries not only affect the price of risk assets around the globe, but also provide investors with real yield, liquidity, and a disinflation/deflation hedge when economies are contracting. Because Treasuries have increasingly become “administered” markets they are mispricing risk, provide no real yield, could become less liquid and may no longer provide portfolio diversification based on their fundamentals.

We need to both construct our portfolios differently and alter our holding periods in response to the risks created by US Treasury market distortions.

Treasury Mispricing

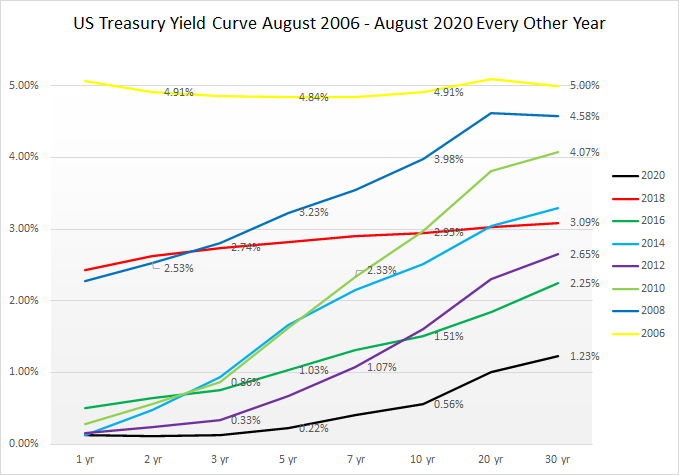

Looking at the yield curve every other year going back to 2006 illustrates how the nominal returns of various treasury maturities has ratcheted down over time.

For real estate or stock market investors, Treasury mispricing becomes obvious when, instead of quoting Treasuries in terms of yield we quote them as a Capitalization Rates (cap) or Price to Earnings Ratios (P/E). Suddenly you see that in 2020 a ten year Treasury is trading for a .6 cap and a P/E of 179 (vs. a ~5 cap and a P/E of 20 in 2006). A 30 year Treasury is trading for a 1.2 cap and a PE of 81 (vs. a ~5 cap and a P/E of 20 in 2006). Because these are nominal yields, inflation could decimate the future the value of these intermediate or long-term treasuries. Why does this matter?

It matters for two reasons.

1. US Treasuries trading at such low yields distorts the value of every other asset on earth rendering many investment strategies in riskier assets dangerous, because small increases in Treasury yields decimate the terminal value of these riskier businesses/assets. The cash flows generated in a typical holding period simply are not enough to offset the reduction in value of an asset or business upon its sale.

2. 99% of financial plans allocate to intermediate and long-term treasuries in an effort to reduce portfolio risk even though Treasuries no longer deliver a positive real return. Because few holders intend to hold them to maturity there is principal risk upon resale. They increase portfolio risk.

How do we replace the role of long-term treasuries in our portfolio in a distorted risk free rate world? That is, how do we achieve a positive real return, liquidity, minimal reinvestment risk, and deflation/disinflation hedge?

Invest in a combination of real estate assets and in loans secured by real estate. I will construct a two part investment that captures the bulk of the historic benefits of Treasuries from a top down perspective and leave bottom up deal sourcing/specifics for another time.

Part One: Direct Real Estate Ownership—For positive real return and minimal reinvestment risk

- If you believe bonds are overvalued, how do you short bonds/interest rates while limiting your exposure if you are wrong?

Purchase a large multifamily asset and borrow at long term fixed rates! Here are some highlights of Housing and Urban Development’s (HUDs) 223(f) program:

- Up to 80% loan to value

- Minimum 1.176 Debt Service Coverage Ratio

- 35 year term

- 35 year amortization

- Non-Recourse

- Assumable

- 2.5%-3% interest rates (as of mid 2020)—in other words premiums of only 150-200 basis points to 30 year Treasuries but with a longer term

- Negotiable 10 year stepdown prepay

- Location Agnostic

The 35 year fixed rate term of the HUD loan accomplishes two things.

1. A HUD loan allows the borrower to effectively short interest rates. The longer a bond’s maturity, the greater its price sensitivity to changes in interest rates making a HUD loan a perfect means to express a belief that interest rates will rise.

2. The term of the HUD loan provides ample time for rents and therefore the asset value growth to more than offset contraction of asset value from rising interest rates. Inflation erodes the real fixed “cost” of monthly mortgage payments.

Principal Agent conflict explains why few real estate syndicators use HUD loans.

- They are difficult to use for purchase money loans as they require months to put in place

- The 35 year term turns off both Limited Partners (LPs) and General Partners (GPs). LPs have been conditioned to believe that they should focus on recycling their capital. But selling a property creates transactional cost and tax friction.

- Imagine selling apartments for $6M that had a $3M loan in place and investors had an initial $1M in capital in place. Let’s assume an LP is only subject to 20% federal capital gains tax. The capital gain is $2M less brokerage/title/escrow fees of $240,000 (4%) equals a capital gain of $1,760,000 creating capital gains taxes of $352,000. The net profit after taxes is $1.4M. 30% of the gain has slipped through the investor’s fingers!

- GPs face the same tax dilemma. However, by realizing the gain the GP can market the high gross exit price and raise even more capital next time around having further established a track record.

- Your edge here vs. 99% of investors is having a longer holding period

Risks: liquidity, political/legal (managed by building a geographically diverse portfolio and due diligence)

Part Two: Make Loans Secured by Real Estate—For low correlation with the stock market via deflation/disinflation hedge, liquidity and real returns

Invest in private money first trust deeds (mortgages) secured by real estate with 1-3 year terms. By making several private money loans with varying maturity dates you create a ladder of self-liquidating bonds. Purchasing longer dated Treasuries and selling them when liquidity needs arise does not work in a rising interest rate environment as a tool to pick up yield because small increases in interest rates can wipe out an entire year’s worth of interest. These private money first trust deeds could be bridge loans to multifamily operators or fix and flip loans secured by single family homes. You will earn high single digit to low double digit expected nominal returns.

If private money first trust deeds capture all of the benefits of a long-dated Treasuries why not strictly invest in them? Firstly, a portfolio of shorter-term bonds will do reasonably well in an inflationary environment. Inflation won’t kill your returns, but inflation won’t help your returns either because you can’t reprice bonds in response to inflation as quickly as you can reprice apartment rents. The second risk is, should the world decide that our currency is being debased at an accelerating rate, that inflation is rising and that real returns on treasuries are negative, more capital may flow into private money mortgages eroding their future returns. Because these investments are self-liquidating there’s always a reinvestment risk. In other words, you need to put your money back out on the street every time a loan matures.

Risks: Credit, prepayment, reinvestment risk, political/legal (managed by not lending to consumers)

Conclusion: Why Does this Two Step Investment Make Sense Now?

- It captures the historic benefits of long-term Treasuries while avoiding their risks today. Granted we lose liquidity vs. long-term Treasuries but this can be offset with an allocation to short term treasury bills.

- Interest rate risk and reinvestment risk oppose one another, therefore owning a multifamily asset with a HUD loan while making private money first mortgages offsets risks.

- HUD loans are not currently pricing in future inflation. They are pricing in about 150 basis points of default risk on the underlying asset they secureYou can’t buy life insurance on your deathbed and you won’t be able to take advantage of distorted pricing in the HUD market if the Department of Housing and Urban Development alters their underlying guidelines or after the United States Department of the Treasury loses control of the bond market.

- In March of 2020, Wall Street pulled way back in the hard money loan market improving the pricing and underwriting criteria for the remaining private money lenders in the market.

I will immediately grab your rss feed as I can not find your e-mail subscription link or newsletter service. Carry Willem Toombs

Pretty! This has been a really wonderful article. Thank you for providing this information. Mable Gustavo Redvers