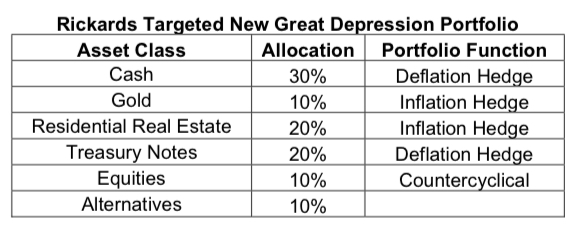

I recently read James Rickards book: The New Great Depression, Winners and Losers in a Post Pandemic World. Rickards lays out his portfolio allocation for this current time period, what he calls the New Great Depression. Here’s the portfolio:

While I personally try to avoid macro calls, looking at his portfolio allocation got me thinking about my own portfolio. Unlike a portfolio of public securities, repositioning a portfolio with a heavy mix of privately held assets takes time.

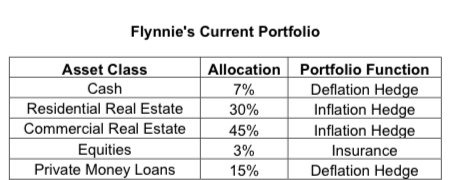

Here’s a snapshot of my current portfolio:

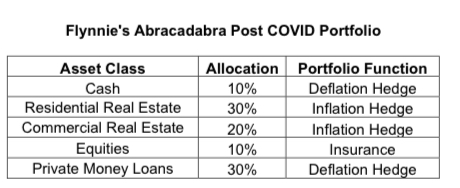

My allocation to Commercial Real Estate has been falling over the last five years as I’ve sold commercial real estate. I have reallocated first into nonperforming loans, and later when COVID hit, into hard money (performing first mortgage) loans. If I could snap my fingers and say “Abracadabra,” reallocating my existing assets into my ideal portfolio, this is would it would look like:

Each asset class here plays one of three roles in the portfolio:

- A procyclical inflation hedge

- A counter-cyclical short-duration deflation hedge

- Longer duration/insurance. By insurance what I mean is a backup source of funds to make sure that I have sufficient dry powder to close on all hard money loans I commit to. I’ll delve more into my equities portfolio in the future, as it becomes more material.

By reducing my exposure to commercial real estate and increasing my allocation to cash, shorter-term private (hard) money loans, and equities, these changes to my portfolio create a far more liquid portfolio.

While I call this an Abracadabra Portfolio, the reality is, that I can’t just snap my fingers and reallocate. I still have, for example, interests in a couple of mobile home parks that still need to be repositioned before they can be refinanced or sold. The $64 question is, will I be able to continue to divest commercial real estate at attractive enough values over the next 6-12 months?

Did you enjoy this article? You can share on Twitter by clicking HERE

Recent Comments